What Is General Average in Maritime Insurance

General Average is a principle in maritime insurance where a deliberate sacrifice of part of a ship or its cargo is made to save the entirety in the face of peril. This concept has ancient origins, tracing back to the Lex Rhodia, a maritime law over 2,000 years old. The modern framework governing General Average is established by the York-Antwerp Rules of 1890. According to these rules, if a ship faces a common danger and part of its cargo or equipment is intentionally jettisoned to prevent disaster, the resulting loss is collectively borne by all stakeholders. The distribution of costs is proportionate to the value of each party’s saved goods.

The implementation of General Average requires decisive action by the ship’s captain or responsible authorities, often during critical situations such as storms where cargo may be discarded to stabilize the vessel. Following such a decision, a specialized adjuster evaluates the situation to determine the financial contributions required from each stakeholder, ensuring that the losses are equitably shared among those whose cargo was preserved. This process not only distributes the financial impact but also underscores the communal nature of risk and protection in maritime voyages.

Additionally, for General Average to be declared, three conditions must typically be met: the sacrifice must be intentional, reasonable, and successful in terms of contributing to the safety of the ship and remaining cargo. Understanding these criteria and the process helps those involved in maritime operations prepare for and respond to such scenarios effectively.

What Does General Average Cover in Shipping

General Average in shipping is a principle where all parties involved in a sea voyage (cargo owners and shipowner) share the financial burden of losses, damages, and additional costs incurred during emergencies at sea.

- Cargo Thrown Overboard: This includes cargo that is deliberately jettisoned to stabilize the ship during dangerous situations like severe storms. The action is taken to prevent the ship from sinking or capsizing.

- Damage to Ship or Cargo: This covers the costs arising from damage to the ship or the remaining cargo due to emergency actions taken to save the vessel. Examples include water damage from firefighting efforts or structural damage from navigating through perilous conditions.

- Extra Expenses: Additional costs incurred as a direct result of taking refuge from adverse conditions are covered. This includes docking and port charges necessary to ensure the safety of the ship and its cargo.

- Salvage Charges: Fees paid to salvage operators who assist in rescuing a ship and its cargo from distress situations. Salvage operations are crucial for preventing a total loss and often involve complex and costly measures.

- Firefighting Expenses: Costs associated with extinguishing fires on the ship, which may involve onboard resources, assistance from other ships, or services from specialized firefighting vessels.

- Tugboat Fees: Costs for services of tugboats are covered when a ship cannot navigate by itself due to damage or mechanical failures and needs towing to safety.

- Temporary Repairs: Immediate costs for repairs to make the ship seaworthy enough to reach the nearest port for comprehensive repairs. These temporary measures ensure the continuation of the voyage with minimal risk.

- Legal and Administrative Costs: Expenses related to the legal and administrative processes of declaring and handling a General Average situation, including fees for average adjusters who assess and allocate the shared costs.

- Security Measures Against Pirate Attacks: Costs associated with both proactive and reactive measures to defend the ship against pirate attacks, including hiring armed security personnel, installing security equipment, and operational adjustments to navigate away from high-risk areas.

In General Average, the value of the saved goods is taken into account when allocating costs. Owners of the saved cargo contribute to the shared expenses proportionally to the value of their goods. This equitable distribution ensures that all parties bear a fair share of the costs necessary to save the voyage.

Who Are The Beneficiaries of General Average

The General Average principle benefits a wide range of stakeholders involved in sea voyages by fairly distributing the costs associated with emergency actions. Here’s a detailed look at who benefits:

Direct Beneficiaries

- Shipowner: The shipowner gains from General Average as it enables them to take necessary emergency measures without bearing the financial consequences alone. When the ship needs saving from dangers like grounding or fire, the costs are shared among all stakeholders, not just the shipowner. This sharing of costs helps ensure that the ship can continue operating, maintaining the business viability of maritime transportation.

- Cargo Owners: Cargo owners also significantly benefit. They receive protection for their investment when their cargo is sacrificed for the safety of the voyage. Rather than suffering a total loss, cargo owners share in the financial impact proportional to the value of their cargo. This arrangement mitigates the financial burden they might face during emergencies, providing a form of collective risk management.

Indirect Beneficiaries

- Insurers: Although they are not directly involved in the navigation or ownership of the cargo or vessel, by spreading the risk among all stakeholders, insurers reduce the likelihood of facing large claims from a single party. This distribution of financial responsibility leads to more manageable and predictable claims, which fits well with insurance models that depend on shared risk.

- Freight Forwarders and Logistics Providers: Freight forwarders and logistics providers gain from the stability and predictability that General Average brings to the shipping industry. By ensuring that no single party bears the financial burden alone in emergencies, General Average helps maintain the continuity of trade routes and shipping services, which are crucial for freight forwarders and logistics providers.

General Average facilitates a structured approach to managing financial losses during maritime emergencies. By distributing the financial burden among all involved parties, it safeguards the economic interests of shipowners, cargo owners and indirectly supports the operations of insurers, freight forwarders and logistics providers, thereby ensuring the ongoing flow of global maritime commerce.

General Average vs. Petty Average

Petty Average covers the more common expenses that occur during a voyage. These are not related to emergencies but to regular operations. Examples include port charges, pilot fees, and minor repairs to the ship. Unlike General Average, Petty Average costs are usually paid by the cargo owners alone, based on their individual agreements. This difference is because Petty Average situations do not involve saving the ship from immediate danger.

General Average protects all parties by sharing the significant risks and costs of maritime emergencies. Petty Average deals with the day-to-day costs of shipping goods. Both are essential for the smooth operation of sea transport but serve different purposes.

The Role of York Antwerp Rules in General Average Practices

The York Antwerp Rules specifically guide the handling of General Average situations in maritime transport. These rules, first established in 1890 and periodically updated, provide a detailed methodology for declaring a General Average, assessing the value of losses and contributions, and executing the distribution process. This includes the valuation of saved and sacrificed property, the appointment of adjusters, and the final calculation of each party’s share. This systematic approach facilitates mutual agreement and cooperation among shipowners, cargo owners, and insurers, minimizing potential conflicts.

The inclusion of the York Antwerp Rules in shipping contracts and insurance policies signifies their importance in global maritime operations. They offer a universally recognized standard that brings predictability and fairness to the resolution of General Average incidents. This not only helps in smooth operational handling but also in fostering trust among international trading partners by ensuring that losses are equitably shared according to a set of predefined, widely accepted guidelines.

The Procedure of Declaring General Average

The procedure for declaring General Average begins when an emergency act is necessary to save a vessel and its cargo. The captain or ship’s master usually makes this critical decision. After the emergency, they must formally announce a General Average situation. This declaration alerts all parties involved: cargo owners, shipowners, and insurers.

After declaring General Average, the shipowner appoints an average adjuster. This specialist calculates each party’s contribution. The calculation is based on the value of their cargo or interest in the voyage. The adjuster assesses the total costs incurred during the emergency and distributes them proportionately. All involved must provide necessary documents about their cargo’s value. This helps in making accurate calculations.

Finally, each party pays their share of the total loss as determined by the average adjuster. This payment process can be complex and might take time to complete. Sometimes, cargo owners may need to provide a security deposit or a guarantee from their insurers. This ensures their cargo is released while financial details are settled. Throughout this process, transparency and fairness are crucial. The York Antwerp Rules guide every step, ensuring consistency and fairness in handling General Average cases worldwide.

Risk of not having General Average Insurance

Not having marine insurance in a General Average event leaves cargo owners vulnerable. They must pay their share of the losses, calculated by their cargo’s value. This direct payment can strain finances, especially if losses are large. Marine insurance offers a shield against these sudden costs.

The logistical side is also challenging. Cargo owners often need to pay a deposit or guarantee to get their cargo back. Without insurance, this upfront cost hits hard. Marine insurance usually covers these deposits, easing the financial burden.

Sea voyages are unpredictable. Weather, mechanical failures, or accidents can trigger General Average. The costs vary widely, leaving uninsured cargo owners facing unpredictable financial hits. Marine insurance adds predictability, allowing owners to operate without constant worry about maritime incidents.

Actionable Steps Following a General Average Declaration

Following a General Average declaration, the initial step for all involved parties is to promptly contact their marine insurance provider. This communication ensures that the insurer is informed about the situation and can begin the process of evaluating the claim. For those who are uninsured, it is vital to understand the impending financial responsibilities.

Next, all parties are required to submit essential documents to the appointed average adjuster. The necessary paperwork typically includes the bill of lading, commercial invoice, and packing list, which are crucial for determining the value of the involved cargo. Insured parties may have this documentation handled by their insurance provider, whereas uninsured parties will need to manage this process themselves. It is important to submit these documents promptly to facilitate a quick resolution and the subsequent release of the cargo.

Finally, all parties must prepare to fulfill the financial obligations as calculated by the adjuster. For cargo owners with insurance, this may involve coordinating with their insurance company to cover the costs. Uninsured owners must arrange to pay their portion of the General Average contribution, which might include securing funds or arranging financial guarantees. Regardless of their insurance status, all parties should remain proactive and responsive to any requests from the adjuster to accelerate the process.

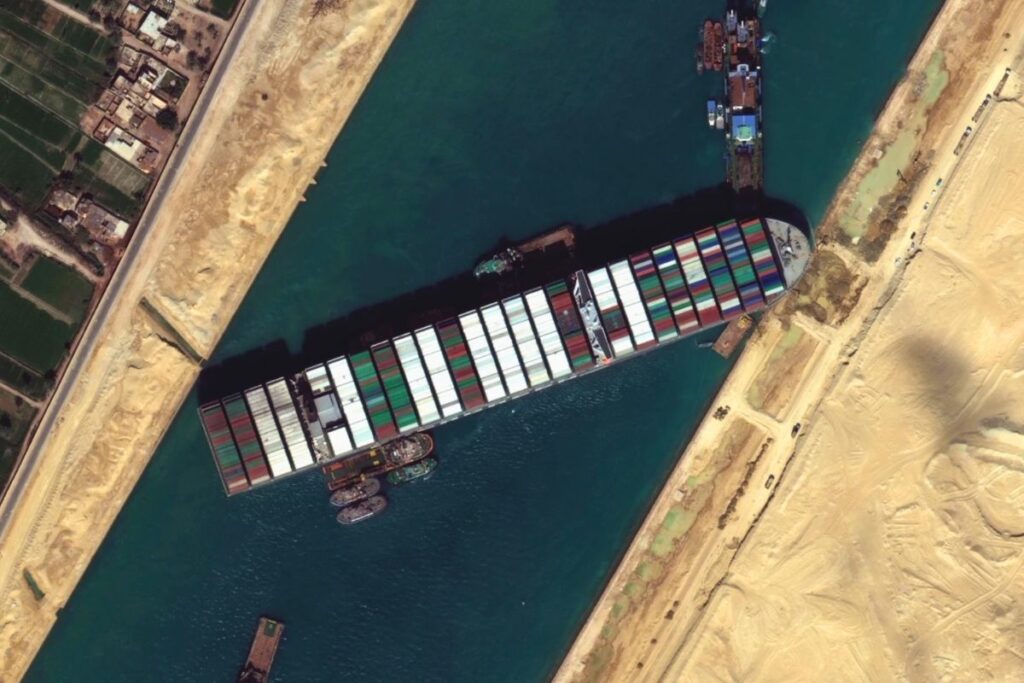

Example When General Average was Declared: “Ever Given incident – Suez Canal”

The Ever Given incident, a major maritime event that captured global attention in March 2021, led to one of the most significant applications of the General Average principle in recent history. The colossal container ship became lodged in the Suez Canal, effectively blocking one of the world’s busiest maritime trade routes for nearly a week. Following the successful refloating of the vessel, the ship’s Japanese owner, Shoei Kisen Kaisha Ltd., and its insurers declared General Average. This declaration meant that the financial impact of the incident and the costs associated with freeing the vessel would be equitably distributed among all stakeholders, including cargo owners and their insurers. The complexity and scale of this situation underscored the vital role of General Average in maritime law and insurance, especially given the Ever Given’s capacity of carrying approximately 18,300 containers and its impact on global trade.

Quantifying the financial impact of the Ever Given incident under the General Average declaration proved to be a difficult task, given the costs involved—from salvage operations and damage repairs to compensation claims and operational delays. Initial estimates suggested that the Suez Canal Authority alone sought compensation of around $916 million, which included salvage efforts and lost transit fees. However, the total General Average expenses were expected to encompass a much broader scope, considering the logistical complications, legal challenges, and the sheer volume of cargo onboard. The cargo ranged from consumer goods and raw materials to critical components for industrial manufacturing, all of which faced significant delays and potential damage.

The declaration of General Average in the Ever Given incident also highlighted the procedural complexities and the need for transparency in the apportionment process. Stakeholders, particularly cargo owners, were required to provide security deposits or guarantees before their cargoes could be released, pending the final adjustment of contributions. This process, governed by the York-Antwerp Rules, involved detailed assessments of the value of saved goods and the proportional allocation of salvage costs, legal fees, and other related expenses. The incident served as a real-world reminder of the challenges and implications of invoking General Average, emphasizing the importance of marine insurance and meticulous documentation for cargo owners navigating the unpredictable waters of international shipping.