The Import Export Podcast

Steve from Coverfreight gives our listeners and understanding of how marine insurance works. We discuss why it’s important for shippers to insure their cargo and who should cover insurance based on the IncoTerms agreed. Steve gives insight into some of the common problems and claims made when shipping goods Internationally. We give tips on how shippers should choose a marine insurance provider for their business operations.

Topics Covered:

- Why is it important that shippers have goods covered by marine insurance?

- Which party should cover the marine insurance? Does it depend on the IncoTerms?

- What are the main types of marine insurance cover? What factors should shippers consider?

- What are the main differences between cover A, cover B and cover C?

- What are the top few major reasons for insurance claims?

- What is the difference between cargo and transit?

- When should shippers consider once-off marine insurance cover VS annual cover?

- How do shippers go through the process of making a marine insurance claim?

- How long would it take from lodging a claim to actually receiving the payout?

- How does Coverfreight work to make marine insurance easy?

What are some key tips to finding a good marine insurance broker?

Listen to Podcast:

Watch Webinar:

Are you working on innovative solutions for the Supply Chain? Contact us for Media partnership opportunities.

Contact UsRead full Transcript here:

Ben: Hi, everybody. It’s Ben Thompson here from incodocs.com. Welcome to the Import-Export podcast. Today, we’re talking about international marine insurance. We’re joined by Steve Mahaffey from Cover Freight. Steve, welcome to the podcast.

Steve: Thank you, Ben.

Ben: So, today Steve and I want to discuss how marine insurance works, what shippers actually need to understand about marine insurance, and how you can ensure that you have the right cover for what you need in your business. So, Steve, before we start, tell me a bit about yourself and the experience you’ve had in this industry.

Steve: Okay, Ben. Well, this is my 25th year in marine insurance. I started off as a marine underwriter at a company called Associated Marine Insurance, a very well-known company here in Australia. I was there for 15 years as an underwriter and various other jobs, working in claims to development, to even management, quite a lot of management. From there, I left the Marine Company and started my own business. I have been now a marine insurance broker for the last 10 years.

Ben: So, you should know a thing or two about marine insurance?

Steve: I hope so. Well, also during that time, I actually did 12 years of study. I ended up obtaining a fellowship in insurance, which is the highest level you can achieve within our industry. And, I also went off to the Australian Maritime College where I got a graduate diploma in ports and logistics.

Ben: Sounds great. So, today, I want to give our listeners some information, just around basic terms, and what marine insurance is, and how it works. So we’ll give them some tips and let them know the best way they can ensure they’ve got the right cover for their business. So, to begin with, I guess, can you explain why it is important that, as a shipper, I must have my goods covered by marine insurance?

Steve: Alright, probably the first and easiest example to explain is the general average incident, where even though your goods might have been damaged on a vessel, if there is some, if their vessel does get into any peril, you have to pay the shipper to get your goods released. So, it’s quite an interesting concept, which I’m sure you’ll probably ask me about later on and I’ll go into a little bit more depths but that’s certainly one reason besides your usual breaking, scratching, denting, chipping, rubbing, bruising, there is plenty of thefts. We have a lot of non-deliveries, containers not turning up, or package is going astray via the various carriers they take it. And then, we also have our major losses of you sinking and stranding, ships getting into trouble. We also have a lot of road rollovers and major losses that occur via that blindside.

Ben: Yes, it’s not so much a straightforward process, is it? I mean, it’s easy for some people to assume that the containers just get delivered. They get put on the boats. They arrive at your door. But, in between, there’s so much risk involved. And it’s imperative that they ensure that cargo because there’d be nothing worse to our business that, as you say, container gets lost or dropped or completely destroyed. That’s a lot of money.

Steve: It’s a lot of money. That’s for sure. Yes, then and I think the actual owner of the goods, they do employ freight forwarders to move their freight around. But, I think a lot of the risk itself, the freight forwarder, certainly doesn’t convey that to the owner of the goods. An example’s like, getting subcontracted to a trucking firm, for instance. And then that trucking firm might subcontract their cargo out to another firm. And then it gets subcontracted out again and finally arrives at your front door in a truck that’s just got white panels on. So, a lot of people were happy just that their goods have arrived but I’m pretty sure they don’t really understand the logistics behind all of that.

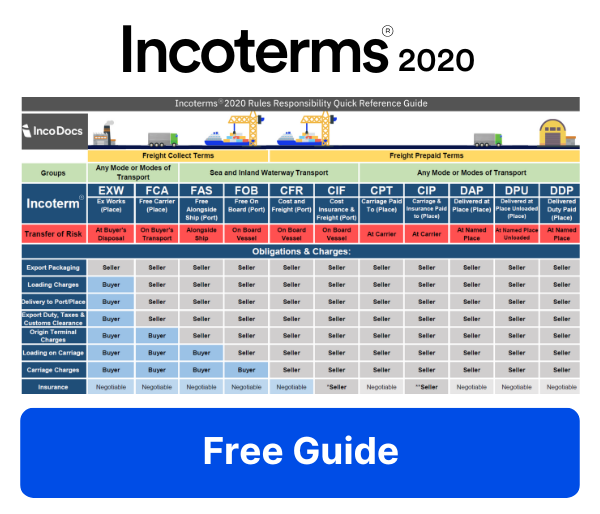

Ben: Yeah, absolutely. And when it comes to who should cover their marine insurance aspect and where the risk changes over, I guess that relies a lot upon the Incoterms, the buyer and seller agree to. So, just say I’m buying 20 foot container from my supplier, and I’ll buy on FOB terms, what’s the best way that I can arrange my cover there? Should I consider, obviously depending on my volume, but what’s the difference between a once-off cover or an annual cover, and the benefits and pros & cons with that?

Steve: For sure, well, marine insurance is all warehouse to warehouse coverage. So, the policy begins once the goods are first picked up for the purpose of loading, and the policy ends once those goods are at their final destination. But, with marine insurance, you need ownership in the goods to actually claim on it. Now, this is an interesting concept for people to get their head around. Now, the ownership is determined by the Incoterms. So, in your instance, where you said you’re importing a container on an FOB basis, the changeover or when you actually own the goods will be at the exporting port overseas, wherever that may be overseas. So, you could say that that first leg because every bit of cargo has to get to the port, that would be the ownership of the seller to you. Now, once you buy the FOB, once it passes the ship’s rail and is on the ship, it becomes the ownership where you can now claim on it. So, and like I said, it will cover it right to the final destination. So, if it arrives here in Australia, for instance, and then it needs to be trucked to the rail and then riled up to the top of North Queensland, that it’ll be in the one marine insurance coverage that you can take out.

Ben: So, it’s important to look into it and get it right and actually understand what part of the journey it actually covers because. . .

Steve: Very much so, yes. Here at Cover Freight, we talk to people about the Incoterms all the time. So, we do have inquiries where people will call up and want insure and we will say, “What’s your term of purchase?” the term of sale that they’re selling it to them. And they might tell us DDP. And, we will tell them that they actually don’t own it until it gets to their warehouse itself. So, there’s no point buying marine insurance.

Ben: Absolutely, so you must so firstly understand the Incoterm properly and then contact your marine insurance provider and get a proper cover.

Steve: Yes, a lot of people confuse payment with ownership of goods in international trade. I would say that’s one of the common areas where we see a little bit of pitfall there that people have a lack of understanding. They think, “I’ll pay for this and so it becomes mine.” Unfortunately, with international trade, it’s all determined by their Incoterm. Some people might have accounts and they might not even pay for those. So, on the reverse side, they might have already have paid for it, they have an account for 45 days with their supplier and the goods have already arrived but their ownership might have been at that FOB point and they need to insure it from then on.

Ben: Absolutely. And what types are the main types of marine insurance cover in simple terms, what, does it depend on the cargo, depend on destination? What are the factors that the shippers should consider?

Steven: Yes, well cargo insurance is one of the oldest insurances around. We’ve always had three types of cover you can purchase under your cargo insurance. Really, the costing now of cargo insurance, the one thing about cargo insurance is that it’s cheap. There’s a lot of competition out there. There’s a lot of competition internationally, let alone here in Australia. There is, I would know at least a dozen underwriters who would offer cargo insurance. So, with that, due to that competitive nature, it’s fairly cheap. And we always recommend people buy the cover A or the top cover. I think you’ll find that the pricing in between, it’s quite pointless to buy what we call an Institute Cargo Clauses C when it might be only $50 to $100 to actually then get an Institute Cargo Clauses A that will cover a lot more risk to your goods.

Ben: So, what are the main differences is split up between cover A, cover B, and cover C.

Steve: Yes, alright. Well, we’ll start at the bottom with cover C. Cover C generally is a major peril cover. What do we call major peril in marine insurance? A major peril is things like sinking, stranding. General average would be a major peril. Once it gets, on the land, a fire or flood or a collision or overturning of the vehicle. We call them your major perils. Cover B, if you buy a cover B, the one in between, will add you a few more sea risks, will add a washing overboard risk to your cover and will also offer some sort of theft element in there as well if you want to purchase an extra theft element. With you cover A, your cover A will cover your full all risk goods, we call it all risks. And in layman’s term, you could use that word, “comprehensive.” So, it’s the most comprehensive cover you can get. So we’ll cover that scratching, denting, chipping, bruising, rubbing, tearing in the container. We will also cover any theft, non-delivery, pilferage if somebody were to steal something out of the container and then seals it back up, and then all your other major perils that are covered under cargo C.

Ben: From your experience what are the top few major reasons for an insurance claim, the most popular, the most popular insurance claims.

Steve: Accidental damage, I would say, would be, if you want to use the word “popular,” would be the most claimed.

Ben: Probably not the right word to use….

Steve: They are certainly the most. Accidental damage is your typical breakage. So, when something isn’t stored correctly in the container it comes loose and it breaks. Or it could be on a flat rack, and it’s gets bumped on another bit of cargo and this leads to accidental damage to it. We certainly have a good sway of the theft claims or non-delivery. It’s hard to say which one. But marine insurance will pay off for either one. And then lightly, I must say, in the last couple of years we’ve had a few general averages come along our shore, which is always an exciting time in our marine insurance claim.

Ben: Yes, it’d be a big job to go through all those claims, no doubt.

Steve: Well, we certainly talk about these major perils and certainly the general average for years and years. We do like it when they come along.

Ben: Yes, okay, and what is the difference between cargo and transit?

Steve: Alright, well, cargo is a term in insurance that’s used to denote any type of goods, produce, livestock, pretty much anything that you can think of that is transported generally for what we call a commercial gain. So, that’s what we would call cargo. We’d certainly, here at Cover Freight, we ensure cargo not for commercial gains, for personal nature, so a household move, for instance, or importing a car. Yes, we certainly do a lot of those but I would say 98% of what we do is for that commercial gain. So, people in trade, buying and selling.

Ben: And, when should I consider doing a once-off marine insurance cover for my shipment or an annual cover? What’re the advantages of either way?

Steve: Yes, well, like I said, the cost of marine insurance has come down substantially. So there has been a shift in annual and single transit policy. There is a shift in the way that, previously, it would cost you the same to buy an annual policy so if you had three single transit policies a year. Now that the price has come down, you could probably do probably half a dozen single transits. And all of that premium together, it would be the same for an annual policy. So, but there’s no doubt about it if you’re an importer or exporter and you’re doing more than, four to eight shipments a year, you can certainly look at an annual policy, because way we see it with marine insurance, a lot of the charges is around the administration. Like I said, marine insurance has been around a long time. It’s been administered very poorly and very costly for the client.

Ben: Yes, okay, and run me through the process of what actually happens if I have a problem with my shipment. I’ve ordered my 20 foor container. It’s turned out to my premises and the cargo has been damaged quite badly. What does that process look like? What’s the first thing I do and how do I claim on that?

Steve: Well the first thing you do is call us here at Cover Freight and we appoint a marine assessor who is on your side. And I know a lot of people think and says, is on your side, but really the assistant’s job is to get all the paperwork, to tell you what to do, to tell you the next steps, to tell you if you can reorder straight away or if you should wait. So, he’s there for that advice on the spot and to run the claim right from the beginning and right through his final recommendations where we pay the client.

Ben: Yes, it’s important to remember, like you said, everybody is working together. You got to jump through the hoops. You’ve got to do fill out the right paperwork. And, typically, how long would that process take from lodging the claim to actually receiving a payment?

Steve: Yes, I would say. Typically, with the industry itself, it would probably around three weeks. We have modernized it quite a lot here at Cover Freight. And, we certainly have, we have what we call settling authority here so we could, we believe in, that can assess the loss. Certainly, any small losses we don’t even bother assessing, we just send out the check and away we go. So, we really don’t want too many hassles with the insurance on the claiming side. We want to make it very easy for the client to get on with their business and put in that reorder and get their stuff back out here. And a lot of policies will even have additional benefits in the event of claims, things like expediting expenses would be included in every single one of our policies. So, if there was something extremely important that was damaged, and it came by sea, and you need it pretty soon, well the policy will pay for air freight to bring the stuff out.

Ben: Okay, yes.

Steve: So, there are a lot of benefits around that claiming situation to try and get you into that same position you were prior to the loss.

Ben: So, it’s important to talk to your insurance broker and give them a really deep understanding of your business.

Steve: Very much.

Ben: They know your operations. They know where you’re buying products from. They know how you’re sending them, air freight, sea freight, how often you’re sending them, where you need to get them delivered to, so that, as you say, in the event of any issues, the cover is already in place and they can go they can go through quite smoothly.

Steve: Yes.

Ben: So, I’ve heard you guys at Cover Freight, you’re working hard to streamline the whole marine insurance cover process. Tell me a bit about how that, what you’re doing, how that works to streamline from making new marine insurance covers to claiming on that online.

Steve: Yes, alright, we’ve worked very hard to put a bit of tech behind this 100-year-old cargo insurance. And, the tech simply scrapes a lot of the information we need in order to produce a quote. It minimizes any sort of, call it errors in double handling, typing errors or whatever it might be. The tech itself sits within freight forwarder’s invoicing systems, all the systems which they use to organize freight from A to B. And what it does is it will scrape the right information out to produce a quote for the freight forwarder then to distribute out to the client itself. The insurance industry back in 2004 went through a reform. They call it the FSRI, which basically excluded a lot of people on selling insurance. So, this tech we’ve developed abides by all the laws out there. So, it’s very difficult around all of those little situations to again allow that freight forwarder to offer cargo insurance to his client even though he’s not a registered insurance broker.

Ben: Okay, yes, I’m sure that would clean up the industry a lot.

Steve: Very, yes, yes. And I guess, we at the Cover Freight, we just want to, not only clean up the industry but also, I would say, shave the pricing off. Because again, like I said, a lot of it’s around the administration with cargo insurance. And now, we’ve pretty much had zero administration.

Ben: Yes, sounds great. So, what are some key tips that we can give listeners when it comes to finding a good marine insurance broker and what to look out for? What sort of tips can you give them to make that process easy?

Steve: Yes. I might say it’s probably a little hard to find a specialist marine insurance broker. Generally, when people leave school they don’t really put their hand up to starting into the insurance industry for one, let alone specialize heavily in probably one of the oldest lines of insurance. So, there’s not too many of them out there. So, you really want to look around for a good specialist when you saw it. A lot of general insurance brokers, as we call them in our trade, as we’re a group of specialists here, general insurance brokers, they’re a little bit like a GP. You go to them and they’ll do everything. They’re a bit of a jack of all trades. But unlike the GP, where you go in with a sore knee and he refers you off to the knee doctor, your general insurance broker, if you go to him with a cargo theory, he’ll think, “You know, I reckon I can operate on this knee and get a result.” So, you do have to be a little bit careful out there. I don’t want to say anything against my people within my fraternity, good or bad. But, certainly, I would try and seek some sort of specialist and see what experience they have been in marine insurance.

Ben: Yes, I think your idea that the knowledge and specialist knowledge in that product and in that industry, I think is quite important.

Steve: Very much so and it’s disappearing within our insurance industry, as well. So, marine insurance, when you talk about your property, and your liability, and your management liabilities, and all these other products that an insurance broker will sell, marine insurance actually constitutes about 2 to 3% of the whole insurance pool. It’s very small so it’s not focused on too much by your generalist insurance broker. They’d rather go for the big-ticket property accounts and the ones that will have a lot more or they are a lot easier targets to obtain.

Ben: Okay, that’s great. Well, thanks so much for being here today, Steve. I think you’ve given listeners quite a few tips on what to look out for and the different types of cover and how it all works. Yes, thanks very much for your time.

Steve: Thank you, Ben.

Ben: Yes, thanks for listening to the Import-Export podcast. This podcast is brought to you by incodocs.com, where importers, exporters and freight companies connect to make global trade easy.

Questions and answers from this podcast

Why is it important that shippers have goods covered by marine insurance?

It’s essential for shippers to insure their cargo because of various risks involved during transportation. These risks include general average incidents where shippers might have to pay the shipper to release their goods even if they aren’t damaged, potential damage like breaking, scratching, denting, theft, non-deliveries, and major losses like sinking or stranding of ships.

Which party should cover the marine insurance? Does it depend on the IncoTerms?

The ownership of the goods, determined by the Incoterms, dictates who should cover the marine insurance. For instance, under FOB terms, the ownership changes at the exporting port overseas. The buyer would then need to insure the goods from that point onward.

What are the main types of marine insurance cover? What factors should shippers consider?

There are three primary types of marine insurance cover:

Cover C: Covers major perils like sinking, stranding, fire, flood, or overturning of the vehicle.

Cover B: Adds a few more sea risks and offers some theft element.

Cover A: Comprehensive cover that includes all risks, including accidental damages, theft, non-delivery, and other major perils.

What are the main differences between cover A, cover B, and cover C?

Cover C is for major perils. Cover B adds some sea risks and theft elements. Cover A offers comprehensive coverage for all risks.

What are the top few major reasons for insurance claims?

The most common reasons for claims include accidental damage, theft, non-delivery, and general averages.

What is the difference between cargo and transit?

Cargo refers to any goods, produce, or livestock transported, typically for commercial gain. Transit refers to the process of transporting these goods.

When should shippers consider once-off marine insurance cover VS annual cover?

If an importer or exporter is doing more than four to eight shipments a year, they should consider an annual policy. However, with the cost of marine insurance coming down, even those doing half a dozen single transits might find an annual policy cost-effective.

How do shippers go through the process of making a marine insurance claim?

In the event of a problem, the shipper should contact their marine insurance provider. An assessor will be appointed to guide the shipper through the claim process, from gathering paperwork to making recommendations for payment.

How long would it take from lodging a claim to actually receiving the payout?

Typically, the process might take around three weeks. However, modernized systems, like those at Cover Freight, can expedite this process.

How does Coverfreight work to make marine insurance easy?

Cover Freight modernizes the marine insurance process, making claims easier and faster for clients. They provide settling authority, ensuring that small losses are addressed promptly without the need for assessments.

What are some key tips to finding a good marine insurance broker?

It’s essential to discuss your business operations in-depth with your insurance broker. This ensures they have a comprehensive understanding of your needs and can provide the best coverage.