Shipping overseas comes with a list of costs. Duties, tariffs, and taxes are three of the most common. Each one affects the cost of goods in a different way. Knowing how they work is important in understanding the total landed cost, trade documents, and compliance across borders.

What Are Duties, Tariffs, and Taxes?

What Is a Duty?

A duty is an indirect tax imposed on goods that cross borders. When charged on imports, it is commonly called a customs duty. Duties are based on the value, weight, or quantity of the goods. The importer usually pays the customs duty to the local customs authority when the goods arrive. Governments use duties to raise revenue and protect domestic industries.

What Is a Tariff?

A tariff is a type of tax imposed on imported goods. It increases the cost of products from certain countries. The goal is to limit foreign competition and support local producers. The importer pays the tariff to the customs authority at the point of entry. Tariffs often change based on trade agreements or policy shifts.

What Is a Tax?

A tax is a government fee added to goods to raise revenue. In international trade, this includes VAT, GST, and sales tax. These are added on top of duties or tariffs. The buyer or end user usually pays the tax. In most countries, customs collects it when goods enter, or it’s charged at the point of sale.

Key Differences

These three charges often appear together but play different roles in trade. Understanding how they compare can help you manage costs, fill out documents correctly, and avoid compliance issues. Here’s a side-by-side view:

| Feature | Duty | Tariff | Tax |

|---|---|---|---|

| Definition | An indirect charge on goods that are imported or exported | A direct charge on goods imported from another country | A fee added to goods to raise government revenue |

| Purpose | To protect local industries and raise state revenue | To control trade flow and adjust pricing of foreign goods | To fund public services like health or transport |

| Who Pays | Usually the importer, paid to the customs authority | The importer, paid at the port of entry | Often the buyer or end user, collected by customs or at the point of sale |

| How Calculated | Based on product value, weight, or quantity | Based on product value or units, sometimes by country | Fixed percentage (e.g. VAT or GST) applied to total value |

| When Applied | At the time of import or export | At the time of import | At import or during the final sale |

| Shows Up On Docs? | Listed on customs declarations, invoices, and tax forms | Often combined with duties or listed as a line item | Seen on invoices and tax declarations |

| Regional Example | 5% duty on electronics entering Australia | US tariff on steel from China | 20% VAT on imports to the UK |

How Duties Are Calculated

The amount of duty you pay depends on the type of product, where it’s from, and how much it’s worth. Here’s how customs works it out.

Customs Value (CIF)

Most duties are based on the CIF value. That means the cost of the goods, plus insurance and freight to the port of entry. This total is what customs uses to apply the duty rate.

HS or HTS Code Classification

Every product must be matched to aHarmonized System (HS) code. This code tells customs what the item is and which rate to apply. The wrong code can lead to overpaying or delays.

Certificate of Origin

This document shows where the goods were made. If a free trade deal applies, the certificate can reduce or remove the duty.

Country of Origin Influence

Some countries face higher rates due to trade policy. If a product is from a country with tariffs or anti-dumping measures, the duty could be higher. Other countries may be given lower or zero rates under trade agreements.

Sample Duty Calculation

Let’s say a shipment of wine from Australia is entering the US:

- CIF value: $10,000

- Duty rate: 7%

- Duty owed: $10,000 × 0.07 = $700

This is what the importer would pay to US Customs on arrival.

WTO Valuation Methods

If the declared value isn’t clear, customs may use other methods:

- Comparative Value: Based on identical goods sold at similar value

- Similar Goods Value: Based on products that are close in type and use

- Deductive Method: Based on the resale price in the importing country

- Computed Method: Based on production cost, profit, and materials

- Fallback Method: A flexible mix if others can’t be used

What You Need to Know About Tariffs

Tariffs are charges placed on goods entering a country. They raise the price of imported items, often to protect local industries. Tariffs are paid by the importer to the customs authority. They apply to specific goods and can change based on trade policy.

Ad Valorem Tariffs

This is a percentage rate charged on the customs value of the goods. For example, a 10% tariff on a shipment worth $5,000 means the importer pays $500.

Specific Tariffs

This type adds a fixed fee for each unit. It does not depend on the product’s value. For example, $2 per liter of imported wine or $15 per pair of shoes.

Compound Tariffs

These combine both types. You might pay a percentage of the value plus a fixed amount per unit. For example, 5% of the value plus $3 per item.

Retaliatory Tariffs

Governments may raise tariffs in response to trade disputes. These are often temporary but can affect many products. A well-known case was between the US and China, where tariffs were placed on goods like electronics, machinery, and food items.

Example: Solar Panels from China

Solar panels made in China have faced extra tariffs in the US. These were added to counter concerns about low-cost imports harming local producers. In some cases, the total tariff reached over 25% of the shipment value. This made Chinese solar panels more expensive in the US market, shifting demand to other suppliers.

What Counts as a Tax? (VAT, GST, Sales Tax)

Import taxes are different from duties and tariffs. These are general government charges placed on goods. Most countries add them to imports as a way to raise revenue. They can include VAT, GST, or sales tax depending on where the goods are going.

VAT and GST

VAT (Value-Added Tax) and GST (Goods and Services Tax) are common worldwide. They apply to the full value of the goods and are usually charged at the border. The importer pays this tax to customs. In some cases, it’s passed on to the end customer.

Here are some standard rates:

- UK: VAT 20%

- Australia: GST 10%

- Canada: GST 5% (plus local taxes)

These taxes are flat rates and apply to most product types, unless exempt. The rate and rules depend on local tax law.

Sales Tax and Local Charges

Some countries also charge sales tax at the state or province level. For example, Canada has PST (Provincial Sales Tax) and HST (Harmonized Sales Tax). These vary depending on where the goods are delivered. US states also apply sales tax, but the country does not use VAT or GST at a national level.

Importer of Record and Tax Responsibility

The importer of record is the party responsible for handling taxes. This includes applying the correct rate, declaring the value, and submitting payments to customs. In many cases, this is the buyer, freight forwarder, or customs broker. If you’re importing into the EU or UK, you may need a valid VAT number to act as the importer of record.

Where These Charges Appear on Trade Documents

Understanding where import costs are recorded helps avoid errors and delays. Duties, tariffs, and taxes can appear on different documents depending on the setup. Here’s where to look.

Commercial Invoice

The commercial invoice often shows a breakdown of charges. This may include:

- Product description and HS code

- Declared customs value (CIF or FOB)

- Duty and tax amounts

- Country of origin

- Total invoice amount including all fees

In some cases, only the product cost is listed. The rest is paid separately by the buyer or freight forwarder. Always check the terms agreed in the Incoterms.

Bill of Lading

The bill of lading does not show payment amounts. It acts as a transport record and proof of shipment. It lists the importer of record, who is the party responsible for customs charges. This is key for assigning payment responsibility.

Customs Declaration / Packing List

The customs declaration includes all key cost elements. This is where customs authorities check the value, origin, and classification. The packing list supports the invoice with item counts, weights, and dimensions, but usually does not show duty or tax amounts.

Certificate of Origin and How It Affects Rates

A certificate of origin is a document that shows where a product was made. It plays a big role in how much duty or tariff is charged.

If a trade agreement exists between the exporting and importing country, the certificate can qualify the goods for lower or zero duty. Without it, the full rate may apply, even if the goods were mostly made in a partner country.

How Origin Affects Duties

Some countries face higher import costs because of trade policy or restrictions. Others get lower rates under free trade agreements.

For example:

A product that’s 60% made in Vietnam and 40% made in China can be declared as made in Vietnam. This allows the importer to avoid tariffs placed on goods from China. The duty rate changes based on the country listed on the certificate of origin.

To claim lower duty, the document must be correct and match the product’s true origin. Customs will often ask for proof, especially if a reduced rate is claimed.

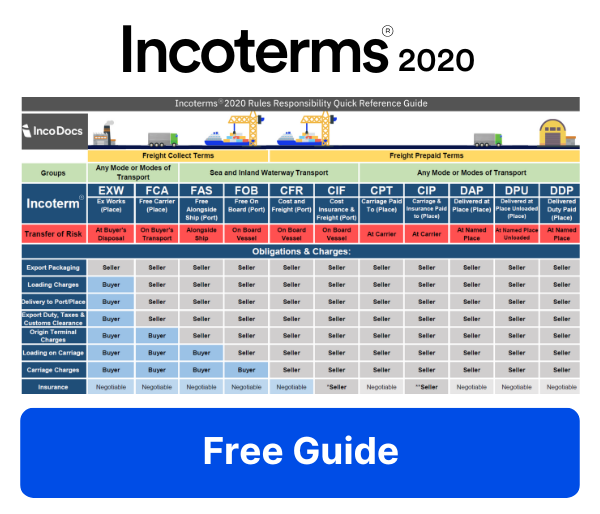

Incoterms and Who Pays What

Incoterms define who is responsible for costs and risks during shipping. Out of the 11 terms in Incoterms 2020, only one makes the seller responsible for all import costs. This includes duties, tariffs, and taxes.

When Does the Seller Pay for Everything?

DDP (Delivered Duty Paid) is the only Incoterm where the seller pays for

- Freight

- Insurance

- Customs clearance

- All import duties, tariffs, and taxes

The buyer receives the goods with no extra charges at the border. The cost for this service might a bit higher but it takes the hassle away for the buyer.

How Foreign Trade Zones Affect Duty, Tariff, and Tax

A Foreign Trade Zone (FTZ) is a special area inside a country where goods can be stored, processed, or assembled without being subject to normal import charges.

Goods inside an FTZ are not treated as formally imported. That means:

- No duties or tariffs are paid while the goods stay in the zone

- No taxes like VAT or GST are charged until the goods leave the zone and enter the local market

- If the goods are re-exported from the FTZ to another country, no import charges apply at all

This setup helps importers delay or reduce costs, especially for goods that are:

- Repackaged or assembled before export

- Held in storage while waiting for distribution

- Mixed with other components to change classification

Before You Ship

Every shipment comes with more than just freight. Tariffs, duties, and taxes shape what you pay and how fast things move. Knowing what applies before you ship saves time, cuts costs, and helps you plan with confidence.

For more insights on trade documents and global shipping, check out the IncoDocs blog.