A letter of credit (LC) is a financial instrument used in international trade. It is sometimes called a documentary credit or a bank commitment. An LC is issued by a bank on behalf of an importer. It guarantees that the exporter will get paid once the required documents are presented. (source: trade.gov)

Banks do not inspect the goods. They only review the documents listed in the LC. This makes it important for exporters to follow the exact terms and conditions set out in the agreement. If the documents match, the bank must release the payment.

For exporters, an LC reduces the risk of non‑payment. For importers, it proves their creditworthiness and allows them to negotiate better payment terms. Together, this creates trust and helps both sides complete more trade deals.

TLDR: Key Takeaways on Letters of Credit in International Trade

- A letter of credit (LC) is issued by a bank on behalf of an importer and guarantees payment to the exporter once required documents are presented.

- Banks check documents, not goods. Even small errors in paperwork can delay or block payment.

- The four main LC types are revocable, irrevocable, confirmed, and unconfirmed, with irrevocable LCs being the most widely used.

- Common required documents include a bill of lading, commercial invoice, packing list, certificate of origin, and insurance certificate.

- Under UCP600 rules, most LCs are irrevocable and must follow strict timelines and document checks.

- In U.S. trade finance, LCs are common for goods, while bank guarantees are often used for projects and services.

How Does a Letter of Credit Work Between Buyers and Sellers?

A letter of credit works by involving both the exporter’s and the importer’s banks in the trade transaction.

Here is the step‑by‑step process:

- The importer and exporter agree on a sales agreement.

- The importer applies for a letter of credit from their issuing bank.

- The issuing bank drafts the LC and sends it to the advising bank in the exporter’s country.

- If needed, a confirming bank adds a second guarantee for extra security.

- The exporter ships the goods. A freight forwarder may assist with transport and paperwork.

- The exporter submits documents to their bank. These include the bill of lading, invoice, and other required documents.

- The advising or confirming bank checks the documents for compliance with the LC terms and conditions.

- If the documents match, the bank releases payment to the exporter.

- The issuing bank then gives the documents to the importer, who uses them to claim the goods.

The Four Main Types of Letters of Credit

Letters of credit are divided into the four main types most often used in international trade. Exporters and importers may also encounter other forms designed for specific trade needs.

Revocable Letter of Credit

A revocable LC can be changed or cancelled by the issuing bank without asking the exporter. This creates a high level of risk for sellers. Because of this, revocable LCs are almost never used in modern trade. Exporters usually avoid them as payment is not secure.

Risk Level: High for the exporter

Irrevocable Letter of Credit

An irrevocable LC cannot be cancelled or altered unless all parties agree (the importer, exporter, and issuing bank). It provides strong protection for exporters because the bank is bound to pay once documents meet the terms. This is the standard form used in most international transactions today.

Risk Level: Low for the exporter

Confirmed Letter of Credit

A confirmed LC adds a second guarantee from another bank, often in the exporter’s country. This is common when the exporter does not fully trust the importer’s bank or when the importer is based in a high‑risk country. The confirming bank promises to pay even if the issuing bank fails. It gives exporters extra security but usually comes with higher bank fees.

Risk Level: Very Low for the exporter

Unconfirmed Letter of Credit

An unconfirmed LC relies only on the issuing bank’s guarantee. It is less secure for the exporter but faster and cheaper to arrange. Exporters may agree to an unconfirmed LC if they trust the importer’s bank or if the trading relationship is well‑established.

Risk Level: Medium for the exporter

Comparison Table of the Four Main Types

| Type of Letter of Credit | Security for Exporter | Typical Use | Risk Level |

|---|---|---|---|

| Revocable LC | Very low | Rarely used today | High |

| Irrevocable LC | High | Standard in international trade | Low |

| Confirmed LC | Very high | High‑risk markets or uncertain banks | Very Low |

| Unconfirmed LC | Moderate | Trusted banks or established partners | Medium |

Other Different Types of Letters of Credit

Exporters and importers may also use other forms depending on their situation:

- Letter of Credit at Sight: Payment is made immediately once the exporter submits correct documents.

- Deferred Payment (Usance) LC: Payment is made later, often 30 to 90 days after shipment.

- Standby LC: Works as a safety net if the importer fails to pay.

- Transferable LC: Lets the exporter pass the credit on to another supplier.

- Back‑to‑Back LC: Uses one LC as security to issue another, often for paying suppliers.

- Revolving LC: Credit renews automatically for ongoing shipments.

- Red Clause LC: Provides the exporter with an advance payment before shipping.

- Green Clause LC: Similar to a red clause LC but also covers storage and insurance costs.

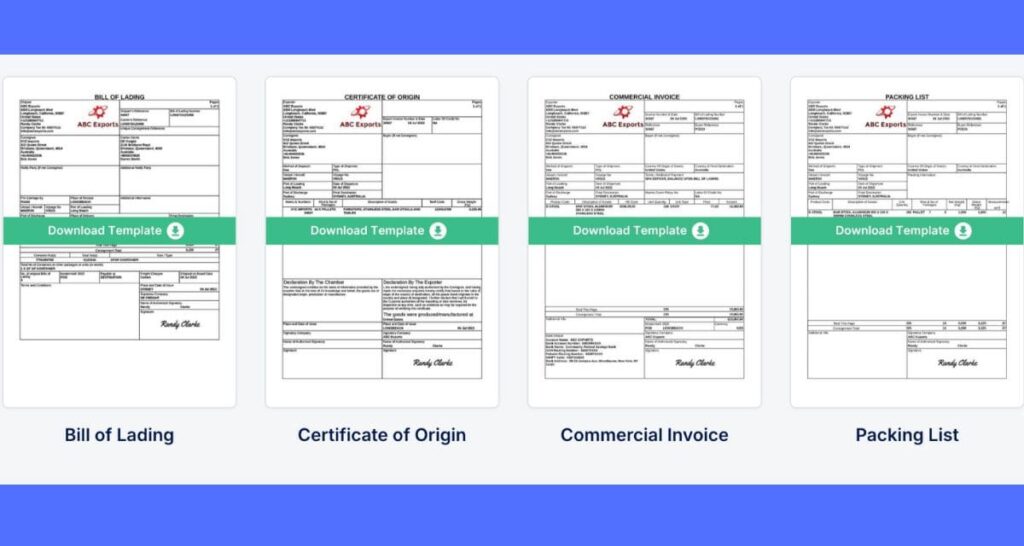

Documents Required for a Letter of Credit

Every letter of credit (LC) relies on strict paperwork. Banks only release payment when all required documents match the terms and conditions specified in the LC.

Exporters usually need to provide:

- Bill of Lading

Confirms shipment of goods. It allows the importer to claim the cargo. - Commercial Invoice

Lists the value, terms, and details of the sale. - Packing List

Provides details about the contents, weight, and packaging of the goods. - Certificate of Origin

States where the goods were produced. Some U.S. exports need this for customs clearance. - Insurance Certificate

Proves the goods are covered during transit. - Inspection Certificate (if required)

Confirms the goods meet the agreed quality and quantity.

Small errors in the LC, such as misspelled names or incorrect dates, can lead to delays or non-payment. The authenticity of the LC and full compliance with the conditions specified in the LC are critical.

Many U.S. exporters work with freight forwarders or trade finance specialists to check paperwork before submission. This reduces the risk of rejection and helps ensure smooth payment under the letter of credit.

Advantages and Disadvantages of a Letter of Credit in Global Trade

A letter of credit (LC) reduces risk in trade by guaranteeing payment once terms are met. The protection is strong, but exporters must follow the conditions exactly.

Quick Overview

| Aspect | Advantages | Disadvantages |

|---|---|---|

| For Exporters | Security of payment from issuing bank. Faster cash flow once documents are approved. Can use the LC as collateral for financing. Ability to sell to new buyers with limited credit history. | High fees charged by banks, often 0.25% to 2% of the contract value in the U.S. Risk of non payment if documents do not match exactly. Preparation of documents can be complex and time consuming. |

| For Importers | Proof of creditworthiness to foreign sellers. Ability to negotiate deferred or flexible payment terms. Assurance that goods are shipped before payment is released. | Must provide collateral or a credit line to the bank. Fees for issuance, advising, and confirming. Dependence on bank timelines and document checks. |

Compliance Framework: UCP600

Most letters of credit are governed by the Uniform Customs and Practice for Documentary Credits (UCP600), created by the International Chamber of Commerce (ICC). Under UCP600, all letters of credit are irrevocable unless stated otherwise, meaning they cannot be changed or cancelled without the consent of all parties. This rule gives exporters stronger protection, since the issuing bank is bound to honour the LC once compliant documents are presented.

Implemented in 2007, UCP600 streamlined earlier rules and introduced clear standards, such as giving banks a maximum of five banking days to examine documents. The ICC also supports UCP600 with the International Standard Banking Practice (ISBP), which helps reduce document discrepancies. As global trade moves toward digitalisation with tools like eUCP, UCP600 continues to provide a consistent framework for reducing disputes and managing risk in international trade.

Source: ICC Academy – Evolution of UCP600 and Its Impact on Documentary Credits

Letters of Credit and Bank Guarantees in International Trade

Both letters of credit (LCs) and bank guarantees (BGs) are undertakings issued by banks to reduce risk in cross‑border trade. While they may sound similar, they protect against different risks.

A bank guarantee is a promise that the bank will step in if one party fails to perform. It is widely used outside the U.S., especially in Europe and Asia. In the U.S., banks often issue standby letters of credit (SBLCs), which serve a similar function to bank guarantees already used in other markets. Bank guarantees can take several forms, including performance guarantees, advance payment guarantees, and warranty guarantees, each designed to secure a specific type of obligation. (source: Investopedia)

By contrast, a letter of credit ensures payment once the exporter submits documents that match the LC’s terms.

Quick Comparison

| Aspect | Letter of Credit (LC) | Bank Guarantee (BG) |

|---|---|---|

| Purpose | Provides payment security to the exporter once LC conditions are met | Protects the buyer or project owner if the seller fails to deliver or meet agreed terms |

| When Used | Common in U.S. trade for goods shipments where sellers want certainty of payment | Often used for infrastructure, construction, or service contracts where performance guarantees are needed |

| Risk Coverage | Focuses on the risk of non‑payment | Focuses on the risk of non‑performance |

| Trigger for Payment | Payment is made after documents are verified for compliance | Payment only occurs if a default, dispute, or failure is proven |

| Typical Costs | Bank fees based on contract value (often 0.25%–2%) | Bank fees depend on risk and contract size |

| Legal Framework | Usually falls under UCP600 for documentary credits | Governed more by local contract law and banking regulations |

Examples of a LC and BG

- Letter of Credit: A U.S. exporter of industrial machinery sells equipment to a buyer in Brazil. The exporter requests an irrevocable LC. Once the bill of lading and invoice are verified, the U.S. bank releases payment.

- Bank Guarantee: A U.S. construction firm takes on a project in the Middle East. The project owner asks for a performance guarantee. If the firm fails to finish, the bank pays compensation.

Key Point: In U.S. trade finance, LCs are the standard tool for goods transactions. Bank guarantees are more common for projects and services. Each reduces risk, but they protect against different problems.

Risks and Compliance Issues Exporters Should Know

Letters of credit help reduce risk in international trade, but exporters still face challenges that can delay or block payment. Most issues come from practical oversights rather than the LC itself.

1. Misaligned sales agreements

If the sales contract and the LC terms are not identical, banks may reject documents. Exporters should review every clause before agreeing to shipment.

2. Unrealistic timelines

Problems often arise when the LC sets a shipping or document submission deadline that doesn’t match production capacity. Negotiating realistic dates upfront avoids costly amendments.

3. Weak issuing banks

An LC is only as strong as the bank that issues it. Exporters dealing with new or high‑risk markets often request confirmation from a U.S. bank to add a second layer of security.

4. Political and currency instability

Sudden events such as sanctions, exchange restrictions, or local banking crises can hold up payments even when documents comply. Using confirmed LCs or trade credit insurance can help manage this risk.

5. Hidden and unexpected costs

Unexpected fees like confirming or amendment charges can reduce profit margins. Agree in advance who covers them.

FAQs About Letters of Credit in International Trade

What is the 4R of credit and how does it relate to LCs?

The 4R framework stands for Right Amount, Right Time, Right Place, and Right Documents. Banks check each before releasing payment under a letter of credit. If even one element is missing or incorrect, payment may be delayed or denied.

In what situations is a confirmed LC recommended?

A confirmed LC is helpful when the exporter does not fully trust the issuing bank or when the buyer is in a high‑risk country. A second bank in the exporter’s country adds its own guarantee, giving extra security.

Who usually pays the fees for a letter of credit?

Fees are often split. The importer usually covers the issuing bank’s charges, while the exporter may pay advising or confirming bank fees. These can range from 0.25 percent to 2 percent of the contract value in the U.S.

Can a letter of credit be transferred to another supplier?

Yes, if the LC is transferable. This lets the exporter pass payment rights to another party, such as a subcontractor or supplier, while keeping the trade secure.