What is Cargo Insurance?

Cargo insurance is an insurance policy that offer coverage for goods while they move through international or domestic transport. It protects shipments against loss or damage during transit and ensures that the value of a shipment is not left at risk. By paying a premium, the shipper transfers the chance of financial losses to an insurance carrier.

Coverage can include risks such as theft, fire, or accidents during loading and unloading. Policies vary in scope, with different coverage options designed for different cargo types and trade routes.

Cargo insurance is different from carrier liability insurance. Liability is capped by law at low limits per package or weight unit, which rarely covers the full value of freight. Dedicated cargo insurance policies are designed to protect shipments at their full commercial value, giving businesses the protection they need.

Why Cargo Insurance Matters

Natural risks in global transport

A container falling overboard in heavy weather is not just a rare story. According to the World Shipping Council, 576 containers were lost at sea in 2024, out of more than 250 million transported. This number is well below the long-term average of about 1,274 containers per year, but it still shows that even a small percentage of loss can impact shippers when it happens to their freight (World Shipping Council).

Flooding in ports and rough seas are not the only natural risks. Air cargo can be damaged during turbulence, while inland rail and road shipments face derailments and collisions. Even well-packed shipments are vulnerable when weather or natural disasters strike. Without insurance coverage, the full replacement cost of lost goods, re-shipping expenses, and delays fall directly on the shipper. With cargo insurance in place, these financial losses can be recovered, and claims are processed so trade can continue.

Theft in supply chains

Cargo theft is not limited to highways. It also happens in container yards, ports, and bonded warehouses. High-value freight such as electronics, luxury items, or pharmaceuticals is often targeted. A single stolen container worth hundreds of thousands of dollars can disrupt cash flow and delay deliveries. A cargo insurance policy that provides coverage for theft protects the business while claims are processed, helping operations continue without absorbing the full financial hit.

Everyday mistakes and accidents

Human error is one of the most common causes of cargo loss or damage. Forklifts can pierce pallets of consumer goods, cranes can drop containers during loading, and fragile cargo may be stacked incorrectly. Even minor mishandling can lead to losses worth tens of thousands of dollars. Cargo insurance covers these physical losses so the shipper is not left chasing the carrier or paying out of pocket.

General average in maritime law

The maritime rule of general average often surprises first-time exporters. When a vessel is in danger, the captain may sacrifice part of the cargo to save the ship. All cargo owners on board are then required to contribute to the loss before their goods are released. Without cargo insurance, this means paying a large bond that can reach six figures just to retrieve a shipment. With insurance coverage, the insurer pays the contribution, and the shipper avoids this unexpected cost.

Liability limits are inadequate

Carrier liability insurance is designed to protect the carrier, not the cargo. It usually pays only a small fixed amount per kilogram or per package, regardless of the actual value of the goods. For example, a container of clothing worth $250,000 might result in a payout of only $10,000 under liability rules. A cargo insurance policy bridges this gap by covering the real commercial value of the shipment and providing financial protection that liability insurance cannot.

Types of Cargo Insurance Coverage Options

Cargo insurance policies are not all the same. The level of protection depends on the type of coverage selected. Below is a summary of the most common options:

| Coverage Type | What it Covers | Typical Use Case |

|---|---|---|

| All-Risks Policy | Physical loss or damage from all external causes except listed exclusions (such as improper packing or delay) | Shippers who want broad protection for high-value or sensitive cargo |

| Named Perils Policy | Covers only specific risks such as fire, sinking, collision, or theft | Useful for shippers transporting cargo with lower value or where only certain risks need to be insured |

| Institute Cargo Clauses (A) | Equivalent to all-risks coverage | Standard option for many international shipments under Incoterms |

| Institute Cargo Clauses (B) | Covers named perils such as fire, stranding, or jettison, but excludes many risks | Often used for bulk cargo where partial cover is acceptable |

| Institute Cargo Clauses (C) | Minimal coverage, usually only for total loss | Cheapest option, but leaves many risks uninsured |

| Open Policy | Continuous insurance that covers multiple shipments over a period | Best for exporters or importers with regular freight movements |

| Single-Shipment Policy | Coverage for one specific shipment only | Ideal for companies that ship infrequently |

| Contingency Policy | Protects the seller if the buyer fails to insure the cargo, even when the buyer was responsible | Common in trade where buyers handle their own insurance but sellers want backup protection |

| General Average Coverage | Pays required contributions when cargo is jettisoned to save a vessel | Essential for ocean cargo shipments subject to maritime law |

Most Popular Cargo Insurance Policies and Coverage Options

All-Risks Policies

This is the most popular option for high-value freight. It provides coverage against almost every external cause of loss or damage, except for specific exclusions like poor packing or delay. Exporters of electronics, machinery, and consumer goods often choose all-risks because one accident could mean a six-figure loss. The higher premium buys peace of mind and quicker claims resolution.

Institute Cargo Clauses (A)

This coverage is widely used in international trade because it aligns with Incoterms such as CIP. It works like an all-risks policy and is recognised by global insurers and brokers. Many banks also require Institute Cargo Clauses (A) coverage when shipments are financed, making it a standard choice for international shipments.

Open Cargo Policies

Frequent exporters and importers often prefer an open cargo policy. Instead of insuring shipments one by one, every shipment within an agreed period is automatically insured. This saves time on paperwork, often reduces premiums through bulk pricing, and ensures no shipment is left uncovered by mistake. It is especially popular with companies running weekly or monthly freight movements.

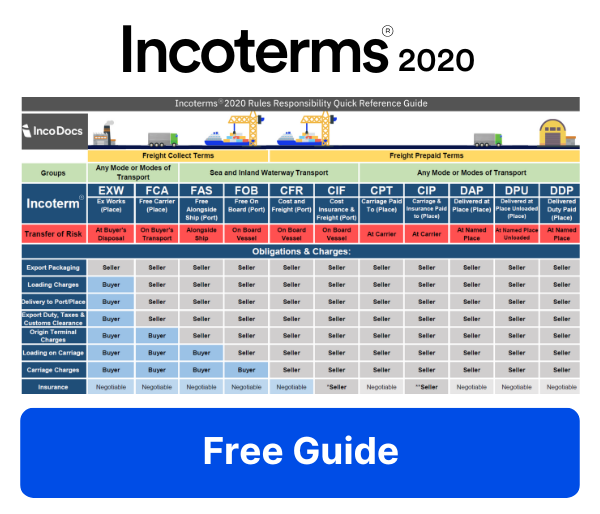

Incoterms and Cargo Insurance Responsibilities

Incoterms do more than set delivery points. They define who must buy insurance, how much coverage is required, and when risk shifts from seller to buyer. The two most common terms tied to cargo insurance are CIP and CIF, but their obligations are very different.

CIP: Carriage and Insurance Paid To

- The seller pays the cost of transport to the named place of destination.

- The seller must provide cargo insurance covering 110% of the invoice value, which is meant to account for both the goods and extra expenses such as administration or lost profit.

- Since Incoterms 2020, CIP requires insurance equivalent to Institute Cargo Clauses (A). This is broad all-risks coverage, giving buyers a high level of protection.

- Risk transfers to the buyer once the goods are delivered to the first carrier. If the buyer wants stronger terms such as a lower deductible, faster claim handling, or war risk cover, they need to arrange this separately with their own insurer.

CIF: Cost, Insurance and Freight

- The seller pays the cost of transport to the port of destination but only needs to buy minimum cover, usually Institute Cargo Clauses (C). This protects against a narrow set of perils like fire, sinking, or collision, but excludes partial losses and many common risks.

- Risk transfers once the goods are loaded on board the vessel at the port of shipment. From that point forward, the buyer carries the risk.

- Buyers using CIF often discover gaps when goods are only partially damaged or delayed. To protect their interests, many arrange an additional cargo insurance policy with broader coverage options.

CIP vs CIF: Insurance Responsibilities at a Glance

| Aspect | CIP (Carriage and Insurance Paid To) | CIF (Cost, Insurance and Freight) |

|---|---|---|

| Who pays freight | Seller pays freight to the named destination | Seller pays freight to the port of destination |

| Who arranges insurance | Seller must arrange insurance | Seller must arrange insurance |

| Minimum insurance required | 110% of contract value, coverage equal to Institute Cargo Clauses (A) | Minimum cover only, usually Institute Cargo Clauses (C) |

| When risk transfers | When goods are handed to the first carrier | When goods are loaded on the vessel at the port of shipment |

| Level of protection | Broad all-risks coverage | Limited named-perils coverage |

| Common buyer action | May add extra coverage if they want lower deductibles or war risk cover | Often buys an additional policy to extend coverage and insure full value |

| Best suited for | High-value shipments, buyers who want strong protection built into the contract | Commodity trades or when buyers are prepared to manage their own additional insurance |

Why shippers must pay attention

A contract using CIF may appear cheaper upfront, but it often leaves the buyer underinsured. In contrast, CIP provides stronger cover but only if the seller has purchased a policy that meets the Incoterms requirement. Misunderstanding these obligations can leave one party exposed. For example, if a buyer assumes the seller’s CIF insurance covers all risks, they may be left with no compensation for partial cargo damage.

Shippers should not only check the Incoterm in the contract but also request a copy of the insurance certificate. Reviewing the insured amount, the type of coverage, and the exclusions ensures the policy actually protects the cargo during transit and storage.

Calculating Insurance Amounts and Premiums

How much should you insure?

Most cargo insurance policies insure the shipment for 110% of the CIF value (Cost, Insurance, and Freight). This ensures that not only the cost of goods and freight is covered, but also extra expenses such as administration fees or lost profit margin. For example:

- Goods value: USD 50,000

- Freight and inland transport: USD 5,000

- Total CIF value: USD 55,000

- Insurable amount: USD 55,000 × 110% = USD 60,500

This insurable amount is what the policy will cover if the cargo is declared a total loss.

How premiums are calculated

Premiums are usually a percentage of the insured amount, often between 0.3% and 0.5%, depending on the route, cargo type, and risk profile. Using the example above, if the premium rate is 0.4%, the cost of insurance would be:

- Insured amount: USD 60,500

- Premium rate: 0.4%

- Insurance premium: USD 242

Some policies have a minimum premium (for example USD 30–50), which applies when the shipment value is small.

Factors that affect the cost

- Type of cargo: fragile, perishable, or high-value items attract higher premiums.

- Transport route: routes passing through high-risk regions for theft or piracy may increase costs.

- Coverage options: all-risks policies cost more than named perils or limited coverage.

- Claims history: shippers with repeated claims may face higher rates.

- Deductibles: a higher deductible lowers the premium, but leaves more cost with the shipper if a claim arises.

How to Buy Cargo Insurance and Work with Brokers

Buying cargo insurance does not have to be difficult. Think of it as a series of steps, each one building on the last.

Step 1: Prepare shipment details

Insurers need specifics: what type of cargo you are shipping, how it is packed, its value, where it is going, and when. Having the commercial invoice and booking information ready avoids delays.

Step 2: Choose the coverage type

Decide how much protection you want.

- All-risks policies are best for high-value or sensitive shipments.

- Named perils policies cost less but only cover specific events such as fire or collision.

- Open policies are ideal for frequent shippers who want every shipment insured automatically.

Step 3: Work with a broker

Most shippers use a specialist broker. A broker compares policies, explains exclusions and deductibles, and helps you avoid paying for gaps in coverage. Ask them what is covered, what is excluded, and how quickly claims are usually paid.

Step 4: Review the policy

Check the insured amount (usually 110% of the CIF value), coverage options, exclusions, and the deductible. If something is unclear, request clarification before you accept the policy.

Step 5: Secure the certificate

Once confirmed, you will receive an insurance certificate. This proves your shipment is insured and is often required by banks, buyers, or customs.

Step 6: File a claim if needed

If cargo is lost or damaged, notify the broker or insurer right away. Provide photos, invoices, and survey reports. Fast action helps ensure claims are settled quickly.

Frequently Asked Questions about Marine Cargo Insurance

How do insurers investigate a cargo insurance claim?

When a claim is filed, insurers first ask for basic documents: the insurance certificate, commercial invoice, packing list, bill of lading or airway bill, and a notice of loss. Depending on the scale of the damage, they may appoint a marine surveyor or loss adjuster. This specialist inspects the cargo, reviews packing and stowage methods, and confirms whether the cause of loss is covered under the policy.

For example, if machinery arrives rusted, the surveyor will check whether it was due to seawater ingress (covered) or inadequate packing (often excluded). Insurers also compare claim amounts with declared cargo values to check for underinsurance. Importers who provide clear photos, survey reports, and prompt notice usually have claims resolved faster, while delays or incomplete documentation often stall settlements.

What cargo types are often excluded from insurance coverage?

Not all goods qualify for standard cargo insurance. Common exclusions include:

- Fragile items like glass, ceramics, and certain electronics if not professionally packed.

- High-risk cargo such as alcohol, tobacco, and precious stones unless covered under a special policy.

- Perishables (fresh produce, flowers, some pharmaceuticals) unless insured with temperature-control clauses.

- Used goods or second-hand machinery, since their condition before shipping is harder to verify.

- Improperly packed cargo where losses are due to poor packaging rather than an external event.

Importers who want to ship these categories can still get insurance, but they usually need to provide extra documentation (for example, packing certificates or temperature logs) or pay a higher premium to reflect the increased risk.

Are premiums different for sea, air, road, and rail shipments?

Yes. Premiums are heavily influenced by the mode of transport because each carries different risks:

- Sea freight: Often higher due to weather events, piracy, and longer transit times. Containerised cargo is generally cheaper to insure than breakbulk.

- Air freight: Premiums can be lower for standard goods since flights are short, but higher for fragile, high-value, or perishable cargo. Theft risk is lower in air but accidents can result in total losses.

- Road freight: Rates vary by region. In some countries, theft from trucks is the single biggest risk. Premiums rise if routes pass through high-crime zones.

- Rail freight: Generally lower premiums than road, but derailments, long transit times, and theft at unsecured yards can push costs up.

Many insurers price multimodal shipments by the riskiest leg. For instance, a sea + road shipment through a piracy-prone region may be rated primarily on the sea risk. Importers can reduce premiums by demonstrating use of secure carriers, GPS tracking, or bonded storage at transfer points.